How-to Compare Financial Advisors

- Matt Garasic, CFP®

- Mar 28, 2023

- 6 min read

Updated: Nov 13, 2023

The State of the Financial Services Industry

The financial services industry is broken. You’re tired of getting sales pitches from people you don’t trust. You’re sick of people using financial slang to try and trick you.

I’m a financial advisor, and I agree. The financial services industry is broken.

That’s why I made the simplest guide you’ll ever read for choosing a financial advisor. Reading this will arm you with everything you need to know to decide what, if any, advisor is right for you.

Investors Don't Trust Financial Advisors

Money influences our happiness, health, relationships, and more.

Something that affects nearly every aspect of our lives shouldn’t be managed by an industry that’s considered as trustworthy as the mechanic who tries to sell us a new engine when we go in for an oil change.

I get it. I really do. But seriously, who ranked politicians 1 or 2?

Financial Advisor Jargon Key

A primary issue is financial professionals use various titles, none of which provide clarity on their business model, compensation structure, or obligation to clients.

Jargon makes my eyes glaze over just as much as you, but you need to understand these terms if you ever want to differentiate advisors.

Registered Investment Advisor (RIA) – the company, not the person who gives investment advice.

Investment Advisor Representative (IAR) – the person who provides investment advice on behalf of the RIA.

Broker-Dealer (BD) – the company that buys and sells securities on the client’s behalf (Fidelity, Merrill Lynch, etc.).

Registered Representative (RR) - the person who transacts securities for clients at a broker-dealer. Commonly referred to as a stockbroker.

The Fiduciary Difference (or not?)

Being a fiduciary or held to the fiduciary standard means you’re required to put your client’s interests above all else.

Without getting into legalities, RIAs & BDs are regulated by different laws.

For decades, RIAs and their reps were subject to the fiduciary standard (strict), and BDs were subject to the suitability standard (less strict) when giving investment advice. Remember this for later.

In 2019, the SEC passed a law that raised the standard of conduct for BDs and their reps. While the new standard isn’t quite the fiduciary standard, both can legally say they’re required to act in their client’s best interest.

Financial Advisor's Conflicts of Interest

Conflicts of interest arise when the potential for personal gain can influence an advisor’s recommendations.

Advisors are required to eliminate/mitigate avoidable conflicts and inform clients of any unavoidable conflicts at the start of the relationship.

Most unavoidable conflicts are a product of the advisor’s business model and/or compensation structure.

For that reason, it’s crucial to understand how transactional, fee-only, and fee-based advisors are paid.

Transactional Compensation

Transactional professionals include registered representatives of broker-dealers and/or insurance agents. Compensation sources may include:

Transaction Costs – costs for facilitating the purchase/sale of a security. These costs reduce the amount of money that gets invested or that you receive after selling.

Ex. Commissions, markups/spreads, sales charges, redemption fees.

Investment Product Payments – payment from an investment company (think mutual fund) for selling their product. You don’t pay these costs directly, but they’re paid from a fund’s assets, which decreases your investment’s value.

Ex. marketing/distribution (12b-1) fees.

Insurance Commission – payment from the insurance carrier to the agent as compensation for selling the insurance product.

Ex: A 7% commission on a $100,000 annuity pays the agent $7,000.

Fee-Only Compensation

Fee-only advisors are IARs at an RIA. However, it must be a fee-only RIA, not a fee-based RIA. Their only compensation comes from fees paid by clients.

Fees may be determined as a percentage of assets under management (AUM), flat fee (sometimes called subscription or retainer), hourly, and/or one-time project fees.

Fee-only advisors charge clients for their advice on investments and other aspects of their financial plan, but they don’t receive commissions or third-party payments for implementation.

Fee-Based Compensation

The term fee-based is an extreme over-simplification, but it essentially means the advisor is paid using a combination of client fees AND transaction, investment product, and/or insurance product commissions.

To earn client fees and investment commissions, an advisor must be registered as both a Registered Representative and an Investment Adviser Representative. These advisors are known as dually registered or dual representatives.

Figure I - a summary of business models and potential compensation sources.

Financial Services Industry Snapshot

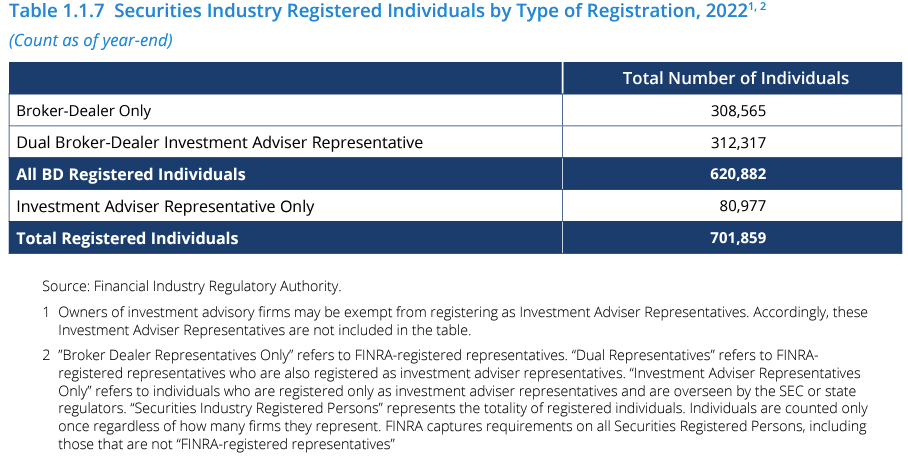

Fee-based models clearly offer the most compensation sources for advisors.

Despite the dually registered model having the most potential for conflicts, Figure II shows that most professionals are capitalizing on the opportunity.

Figure II - 2022 Securities Industry Registration Summary

Source: FINRA 2023 Industry Snapshot

Insurance Conflicts

Unfortunately, I couldn’t find statistics on the overlap of RRs and IARs who are also licensed to sell insurance products, but there’s an important point that requires attention.

Remember when I said IARs and RRs are legally required to act in your best interest when giving investment advice? Well, that requirement doesn’t apply to insurance recommendations.

Insurance recommendations are subject to the suitability standard. This means the advisor must prove their recommendation is suitable for your situation instead of proving it’s in your best interest.

Financial Advisor's Conflicts & Compensation

To be clear, multiple compensation sources and the potential for conflict don’t diminish an advisor’s knowledge, character, or ability to serve clients.

The caliber of service you receive ultimately depends on the integrity of your advisor.

However, more compensation sources typically mean more conflicts and potential for purposeful or unintentional recommendations focused on personal profit over investor success.

Using commonly referenced conflicts/drawbacks of each business model, Figure III highlights how conflicts increase as business models are combined.

Figure III - Advisor Business Models, Compensation Structures, and Potential Conflicts

How Does This Affect You?

Ambiguous fee structures and a lack of transparency limit investors’ ability to evaluate their advisor, quantify their total fees, and recognize if an advisor is acting with poor character.

I believe most advisors are honest, competent, and focused on providing superior client service, regardless of their business model.

However, I also believe clients are more likely to unknowingly have their wealth eroded when exposed to complex webs of compensation and conflicts.

What Should You Do?

As a fee-only advisor, I have a conflict writing this post because I’m biased toward the fee-only model.

However, I’m confident in the logic that identifying an advisor with minimal conflicts and the most transparent business model gives investors the best chance to work with a professional who will place their client’s interests above their own, whose fees are easy to understand, and whose value can easily be measured.

Conclusion

Trust is the most important factor when choosing a financial advisor.

If an advisor discloses their conflicts up front, you’re comfortable with them, and you trust them to act in your best interest, you’re likely in a great position to move forward.

No matter what business model your advisor uses or how they’re compensated, if you ever doubt that they’re acting in your best interest, it’s time to look for a new advisor.

Disclaimer

Unrivaled Wealth Management (“UWM”) is a registered investment advisor offering advisory services in the States of Pennsylvania, Ohio, and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Unrivaled Wealth Management, LLC (referred to as “UWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute UWM’s judgement as of the date of this communication and are subject to change without notice. UWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall UWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if UWM or a UWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

Comments